European banks have reported robust 2025 earnings. European bank bonds have been strongly supported by these solid fundamentals and favorable technical factors, leading to a significant compression of spreads, especially on subordinated debt.

We believe the current fundamental momentum will carry through into 2026. We anticipate net interest income growth potential from the second half of the year, once the central bank rate cuts implemented in 2025 have been largely absorbed by banks.

Consequently, we retain a positive outlook for the banking sector. We believe banks are favorably positioned within an economic landscape marked by, on one hand, a relatively stable macroeconomic baseline scenario, and on the other, an environment replete with numerous underlying risks.

Furthermore, despite stretched valuations and a riskier context, the decline in issuance and the sector's resilience should limit downside risk and support carry. Opportunities remain through mergers and acquisitions, regulation (AT1), and lower capital structure investments.

Healthy fundamentals

The fundamentals of European banks are not a source of concern: they are sound and we expect them to remain so. The asset quality of European banks (and globally) is resilient. The average non-performing loan ratio in Europe remains low at 2.2% according to the European Central Bank (as of Q4 2025).

Non-Performing Loan Evolution: still at historic lows

.jpg)

Capital ratios are solid, with an average CET1 (Common Equity Tier 1) ratio of 16.3% for Eurozone banks according to the European Banking Authority (EBA, Q4 2025).

Net interest income is expected to stabilize through this rate-cutting cycle, with growth potential in the second half of the year, as we anticipate a slight rebound in credit origination. Specifically, we hold a favorable view on the revenue growth of Spanish, Greek, and UK banks, which exhibit loan growth above the European average. French banks, in turn, will benefit from the decrease in Livret A rates, supporting their net interest margins.

Finally, we are constructive on universal and investment banks, which benefit from robust investment banking pipelines and positive inflows in life insurance and asset & wealth management. We project that the performance of these banks will remain robust.

Multiple themes to monitor, short-term and medium-term

Among the most significant and short-term, the subject of banking consolidation remains central. This is particularly true in fragmented banking landscapes, notably in Italy.

Furthermore, German stimulus is key for European growth and loan growth. The growth in Eurozone loan volumes, currently around 2.5%, remains below that observed in the United States and the United Kingdom.

On the regulatory front, several topics persist: notably the introduction of deposit preference within the framework of CMDI (Crisis Management and Deposit Insurance) .

On more structural issues, the banking landscape is becoming increasingly competitive with the emergence of neo-banks. This is pushing banks to accelerate their digital transformation. The development of stablecoins (stable cryptocurrencies) can represent both threats and opportunities for banks that quickly adapt to the digitalization of finance.

Black Swan risk

Despite our favorable view on fundamentals, several risks could challenge our outlook. However, banks have a solid starting point to face these risks.

We are particularly monitoring macroeconomic, political, and geopolitical risks, which are likely to affect growth, inflation, the trajectory of rates, and consequently, loan growth, margins, and asset quality. Banks also remain relatively sensitive to domestic sovereign risk. It should be noted that European banks have very limited exposure to the Middle East but remain exposed to the consequences of the conflict on the economic environment.

The rise of private debt is another risk: defaults observed in September 2025 have raised concerns. European banks' exposures to private debt remain limited and lower than those of US banks. However, with the development of SRTs in Europe particularly (Significant Risk Transfer, a capital optimization tool), we will be monitoring increasing exposure to private debt funds.

Finally, Artificial Intelligence is a major issue: significant investments and high valuations in the Tech sector. Banks' exposure to Tech and software companies (threatened by Articial Intelligence) remains moderate. Banks are more sensitive to a decline in stock markets and a slowdown in Information Technology (IT) investments, which would, however, impact US growth more than European growth.

In addition to benefiting from robust fundamentals, European banking sector bonds have also been supported by very favorable technical factors. Indeed, strong inflows observed in the credit asset class in 2025 (€36 billion in the Investment Grade segment and €9.5 billion in the High Yield segment) have, among other things, helped absorb generally higher volumes of bank 2025 issuances compared to 2024, particularly in the 'senior non-preferred' and holding segments. This appetite for sector issuances remained firm despite near-zero issuance premiums.

As illustrated by the table below, this environment has resulted in a very good year for the sector in absolute terms, but also relative to the Investment Grade credit market, as average spreads over swaps compressed more significantly for senior debt, and even more so for subordinated and hybrid debt (such as contingent convertible bonds - CoCos)

Based on current bank issuance estimates, net issuance volumes for 2026 are expected to register a slight decline, which should again support the sector and complement the still-solid fundamentals. However, 2026, from an investor's perspective, is likely to be more complex, primarily due to very tight valuation levels and risk factors that are difficult to gauge, such as the impact of Artificial Intelligence on the one hand, and the situation of private debt and private equity, marked by a degree of opacity, on the other. Geopolitical tensions also constitute a major risk factor.

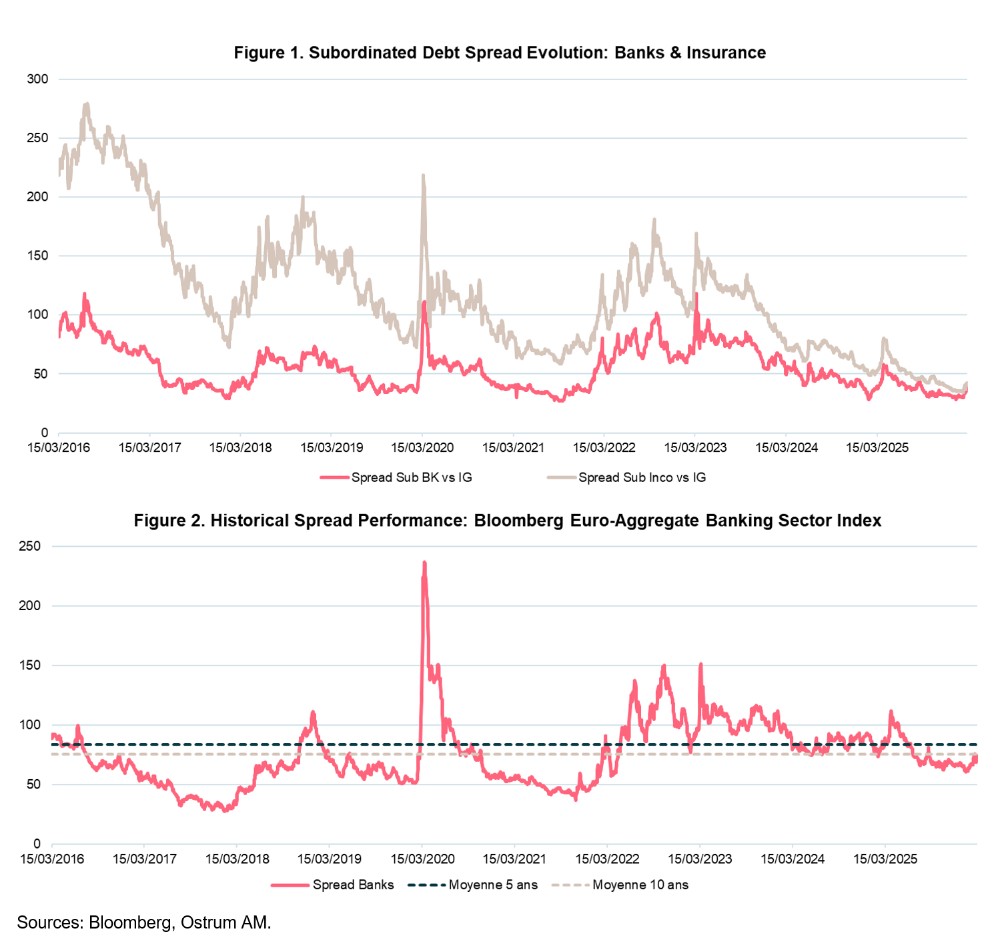

Despite current spreads in the banking sector being below their 5- or 10-year historical averages (see Figure 1), we believe that within Investment Grade financial bonds (excluding the real estate sector), the banking sector could reach new historic lows. This outlook extends to insurance sector debt, at least for subordinated debt where the comparison is most relevant (see Figure 2). The potential for spread tightening on bank debt may be limited, but the sector should offer good carry opportunities. This is because, conversely, barring major systemic events, the risk of spread widening should also be contained due to the previously described technical factors..

Beyond valuation considerations, the banking sector is expected to offer numerous opportunities in 2026. Several themes should invigorate this segment and allow investors to create value. The meger & acquisitions (M&A) theme will likely generate investment ideas, especially as 'golden power' in certain European states comes into question.

The regulatory theme can also create opportunities, particularly for AT1s , whose characteristics might be reviewed by the regulator (potentially creating a positive technical factor for the existing stock). Furthermore, we anticipate continued potential for favorable rating migration (notably into Investment Grade territory) on subordinated instruments of certain banks, including some AT1s.

Finally, with solid fundamentals in banks, it may be interesting to seek investment opportunities further down the capital structure (subordinated instruments). Moreover, we anticipate that the risks of widening on bank subordinated debt will remain low.

Conclusion

European banks hold a significant weighting in Euro credit portfolios, making them a key focus for Ostrum AM. Our favorable outlook for the sector in 2026 supports our intention to maintain a robust exposure to bank securities. Our commitment to thoroughly assessing European bank quality and forecasting market trends is backed by 22 Credit & Sustainability analysts, with dedicated expertise in financial institutions. Their insights inform the banking market research and subsequent investment decisions of our credit management team, which consists of 11 senior portfolio managers.