Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum AM's views on the economy, strategy and markets.

Outlook at 03/20/2026.

The CIO letter

War in Iran sparks an oil price shock

The military campaign spearheaded by the United States and Israel against Iran has ignited a new geopolitical front, emerging in the wake of tensions over Greenland and the US intervention in Venezuela. In response to US and Israeli strikes, Iran has retaliated by targeting energy infrastructure and Western interests across the Middle East. Oil prices have surged above $100, as Iranian authorities closed the Strait of Hormuz. Beyond crude oil, the trade of metals and other raw materials is slowing sharply. At this juncture, a ground intervention remains uncertain. Consequently, maritime traffic is likely to remain disrupted for several weeks, if not months, with the inevitable consequences of higher prices and supply shortages. The resolution of this crisis will hinge on the United States' capacity to secure control of the region while simultaneously mitigating sabotage efforts.

For financial markets, the reaction function of central banks will be a pivotal factor. Preemptive tightening to contain inflation expectations would exert downward pressure on the valuations of growth-sensitive assets. In the US, current labor market weakness might advocate for policy easing, but the prevailing price shock warrants caution. The ECB will maintain a vigilant stance, particularly if inflation expectations drift higher; however, a prolonged status quo remains the most probable scenario. The BoE is in a precarious position, while the RBA has already started hiking. Across markets, risk premiums are on the rise. Ten-year yields have increased in response to higher oil prices. The fiscal cost of the war requires new funding in the US, suggesting that the 10-year Treasury yield will keep hovering around 4.25%. The German Bund may trade near 3% for some time before potentially retreating. Downside financial risk is concentrated in equities; however, many investors have already hedged downside risks. Credit spreads may widen moderately, influenced not only by the ongoing conflict but also by the substantial issuance from hyperscalers.

Economic Views

THREE THEMES FOR THE MARKETS

-

Growth

US growth weakened at year-end with the shutdown and a stalled labor market. The oil price rise will weigh on household consumption, but AI investment is stimulating activity. The eurozone is experiencing a moderate recovery somewhat disrupted by the oil shock. In China, domestic demand shows some signs of stabilization. Investment remains under pressure with the policy of reducing overcapacity. The blockade of the Strait of Hormuz is creating difficulties for production chains beyond oil.

-

Inflation

In the United States, CPI was decelerating (2.4% in February) before the Iranian crisis. The consumption deflator, with less weight on housing, nevertheless remains close to 3%, well above the Fed's target. In the Eurozone, inflation stood at 1.9% in February. However, the rebound in crude oil and the adjustment of the euro will cause inflation to rise in the spring. In China, inflation is recovering from very low levels. Producer price deflation is moderating thanks to rising metal prices and anti-deflationary measures.

-

Monetary policy

The Fed left its policy unchanged in March. A downward adjustment of rates is expected to resume given rising unemployment, despite the inflationary episode. The ECB is expected to maintain the status quo at 2% until the end of 2026, while remaining vigilant about inflation risks. The PBOC might postpone its rate cuts to the second quarter, awaiting more data to gauge the state of the Chinese economy.

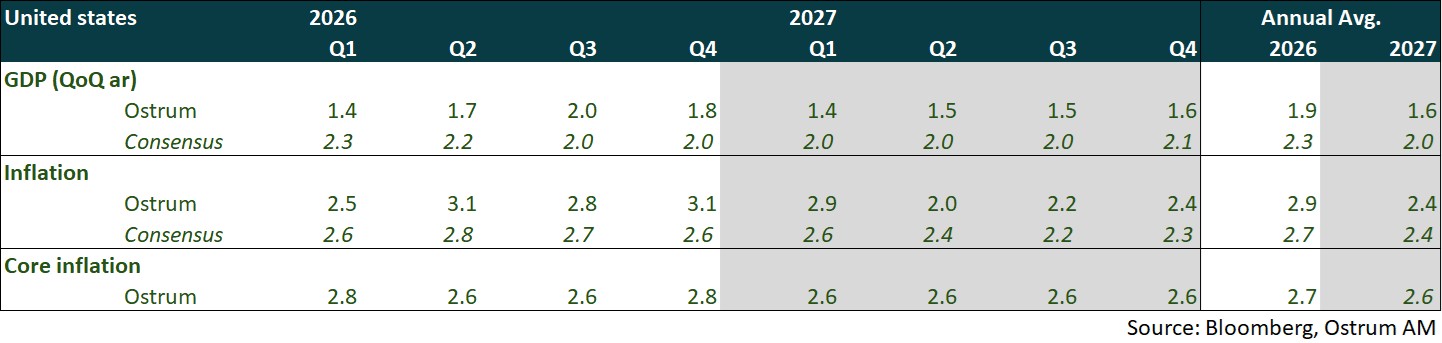

ECONOMY: UNITED STATES

Growth to slow to 1.9% as price shock and labor market weakness impact spending.

- Demand: Household disposable income has been declining for a year, and consumers are enduring the oil price shock. Household credit quality remains poor, although consumption is expected to be supported by the reimbursement of excess tax collections in the first half of the year. The improvement in the trade balance in January is likely to be temporary. Housing investment will contract in 2026, but signs of stabilization are emerging. Productive investment will continue to be primarily driven by AI (data centers, software, and R&D).

- Labor Market: Hiring has stalled. The unemployment rate is expected to exceed 4.5% in 2026, despite low labor force participation. Job openings continue to trend downward, but labor shortages persist in certain sectors.

- Fiscal Policy: As mid-term elections approach, transfers to households are possible, partly offsetting the rise in oil prices. The potential reimbursement of tariffs (approximately 0.5% of GDP) would act as a stimulus benefiting businesses. A budget supplement of $200 billion for defense is under consideration.

- Inflation: Disinflation, primarily linked to housing, is now contending with rising energy and other commodity prices. Tariffs are capped at 15% until July.

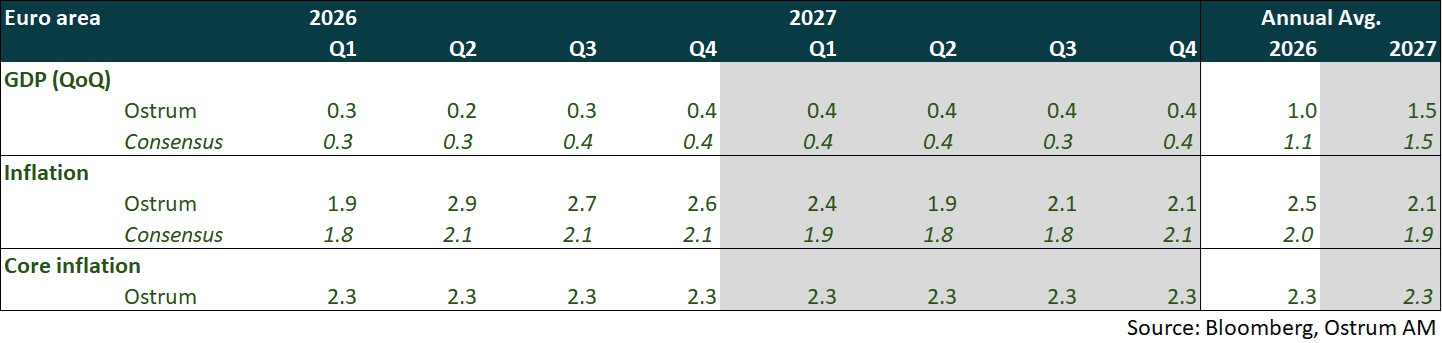

ECONOMY: EURO AREA

The geopolitical conflict in the Middle East introduces greater uncertainty into forecasts, making them dependent on the conflict's duration. The likely persistence of high energy prices in Q2 should have a transient impact on inflation, leading to more moderate growth in 2026.

- Domestic Demand: Rising energy prices are expected to weigh on consumer and business confidence, resulting in somewhat less robust domestic demand than initially anticipated for H1 2026. Some governments are implementing measures to mitigate this impact. This energy price effect is expected to partially offset the positive contributions from German stimulus plans, increased military spending in Europe, and NextGenerationEU disbursements.

- External Demand: Foreign trade is projected to make only a marginal contribution to growth. Tariff-related uncertainty is expected to persist, and Germany will continue to face increased competition from China.

- Fiscal Policy: Germany, after years of fiscal prudence, will significantly increase spending on infrastructure and defense. In France, the budget deficit is projected to remain the highest in the Eurozone in 2026, targeting 5% of GDP. The approaching 2027 presidential election will make compromises even more difficult in autumn 2026, suggesting no immediate fiscal consolidation. Several countries are gradually implementing measures to limit the impact of rising energy prices (Italy, Spain, Portugal, etc.).

- Inflation: After falling below 2% in January and February, inflation is expected to rise significantly from Q2 due to the sharp increase in energy prices (oil and gas) linked to the Middle East conflict. This impact is expected to be temporary, with inflation returning towards the 2% target during 2027. The effect on core inflation should be limited.

ECONOMY: CHINA

Growth in 2025 reached the 5% target, but the beginning of 2026 is rather mixed. Exports remain robust, contrasting with weak domestic demand, particularly in investment. Xi Jinping’s call to make the yuan a reserve currency should support its appreciation against the dollar.

- Net Exports: Growth reached its target thanks to resilient exports, whose contribution (one-third) hit its highest level since 1997. Easing trade tensions (Canada, United Kingdom, Germany(?)) and the move upmarket of exports encouraged by the 15th Plenum (AI, batteries, electric vehicles) should support momentum in 2026.

- Consumption: Consumption shows encouraging signs, as evidenced by the resilience of the RatingDog survey in services. However, limited visibility in the labor market and the real estate crisis remain major obstacles to a broader recovery.

- Investment: Investment posted its first decline last year. Despite the RMB 200 bn plan—about 2% of GDP—to support equipment investment, this was not enough to offset the drop in real estate investment. A new RMB 96 bn plan should provide additional support. However, the amount appears insufficient and may need to be increased. The main challenge for policymakers is to revive private investment, the key source of employment.

- Inflation: Inflation ended 2025 at 0.1%, and core inflation stabilized at 1.2%, the highest in two years. This is positive, as price dynamics have not deteriorated.

- Monetary Policy: The PBOC may postpone rate cuts while waiting for more economic data to gauge the state of the economy.

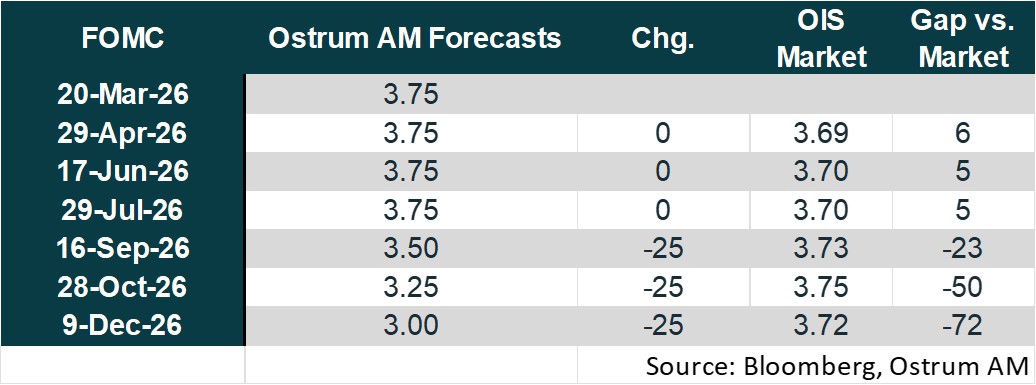

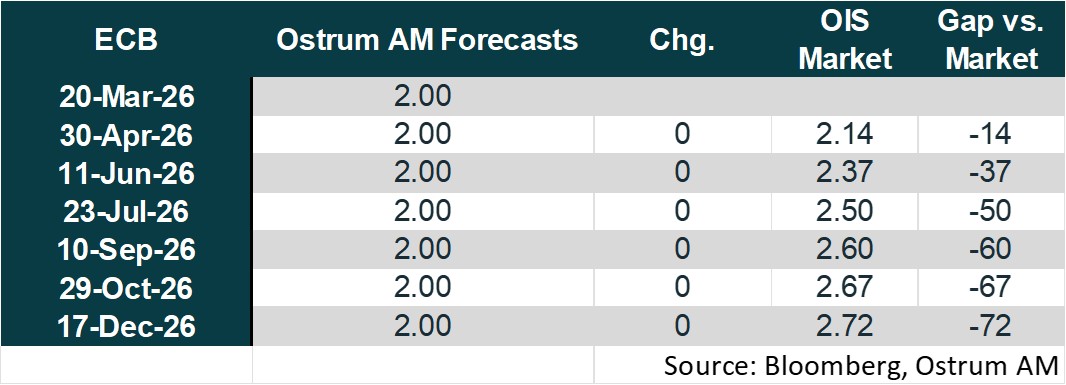

Monetary Policy

Fed and ECB cautious given uncertainty surrounding energy shock

- Fed easing postponed

The Fed kept its rates unchanged for the second consecutive time on March 18. Surprisingly, the central bank continues to describe growth as "solid," despite acknowledging weak job creation and inflation still somewhat elevated. Jerome Powell highlighted the uncertainty linked to the Middle East conflict. Growth forecasts were slightly revised upward to 2.4% from 2.3% for 2026 (Q4/Q4), as were those for inflation (2.7% from 2.4%). The unemployment rate is projected to remain at 4.4% (unchanged). FOMC members continue to anticipate, on average, one rate cut this year and another in 2027. The Middle East conflict further complicates the Fed’s position: higher inflation, at least in the short term, and downside risks to growth and employment. We believe the Fed should prioritize the ongoing deterioration of the labor market and cut rates three times this year, although the timing has become more uncertain.

- A vigilant ECB

The ECB kept its rates unchanged on March 19, marking the sixth consecutive hold. Its updated projections incorporate data up to March 11, thus accounting for some of the energy price surge linked to the Middle East conflict. Consequently, inflation forecasts for 2026 were significantly revised upward to 2.6% from the 1.9% anticipated in December. Inflation is expected to moderate to 2% in 2027 and 2.1% in 2028. Core inflation projections were also slightly revised higher (to 2.3%, 2.2%, and 2.1% respectively), while growth forecasts for 2026 and 2027 were lowered to 0.9% and 1.3%. Christine Lagarde emphasized that the conflict heightens uncertainty and that medium-term consequences will depend on its intensity and duration. In a context of temporary inflation increases stemming from a supply shock, the ECB is expected to keep rates unchanged while adopting a firm tone to effectively anchor long-term inflation expectations.

Market views

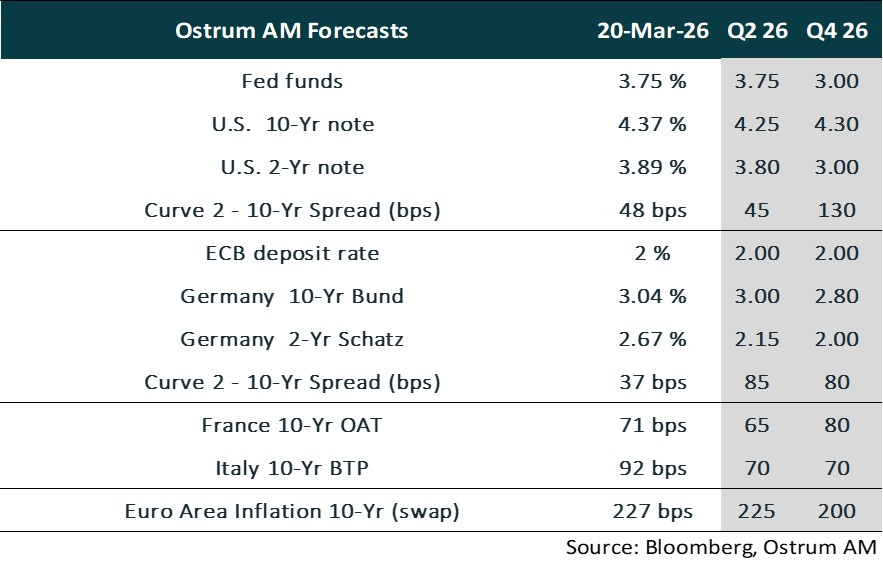

- U.S. Rates: The inflation shock complicates the Fed's task. We anticipate monetary easing to resume towards the end of the year.

- European Rates: The ECB is expected to maintain its current policy rate of 2% but stands ready to intervene should inflation expectations rise. The 10-year Bund yield is projected to fluctuate around 3% before declining towards 2.80% by year-end.

- Sovereign Spreads: Sovereign spreads are modestly higher amid the Iranian crisis. However, political risk in France is expected to weigh on OATs later in the year. Italy's spread is likely to resume tightening, reversing its recent underperformance.

- Eurozone Inflation: Long-term inflation expectations have increased due to the oil price shock. This inflation risk premium is expected to diminish in the second half of the year.

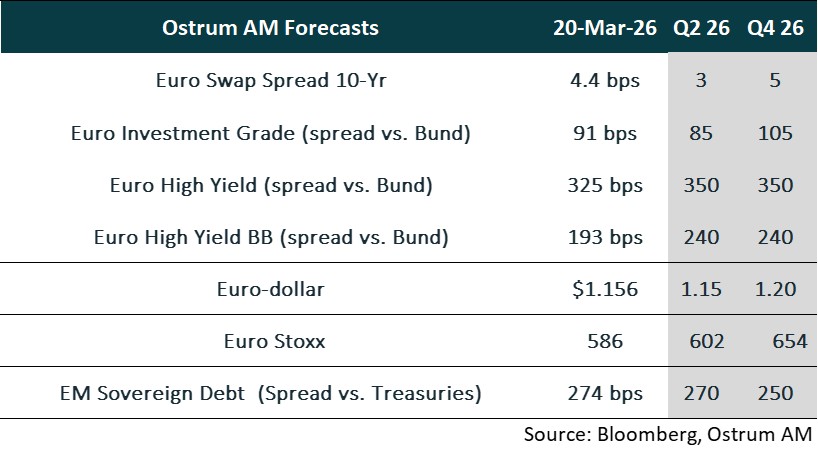

- Euro Credit: Investment-grade credit spreads have demonstrated resilience amidst the Iranian crisis and significant issuance volumes. A gradual normalization of spreads toward higher levels is still anticipated.

- Euro High yield: Valuations in the high yield segment are expected to normalize over the course of the year. However, the default rate remains contained and below average.

- Exchange Rates: The dollar has reasserted its safe-haven status during the Iranian crisis. Nevertheless, the structurally bearish trend for the greenback is expected to resume in the second half of the year.

- European Equities: Equities are being impacted by the energy crisis. Earnings revisions are likely before a rebound in profits and an increase in multiples in the latter half of the year.

- Emerging Debt: The EMBI Global Diversified (EMBIG) is showing resilience amidst the Iranian crisis. The trend of spread tightening is expected to resume.