Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Summary

Listen to podcast (in French only)

(Listen to) Axel Botte’s podcast:

- Review of the week – The ongoing Iranian crisis;

- Theme – March FOMC preview.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: March FOMC preview

- While the Fed kept rates unchanged at 3.50-3.75% in January, circumstances have shifted with the Iran crisis driving oil prices higher, weak employment reports, and heightened financial risks in private credit markets requiring reassessment.

- The U.S. economy added only 6,000 jobs per month on average over the three months through February 2026, with unemployment reaching 4.4%, suggesting the Fed may need to ease policy if conditions continue deteriorating.

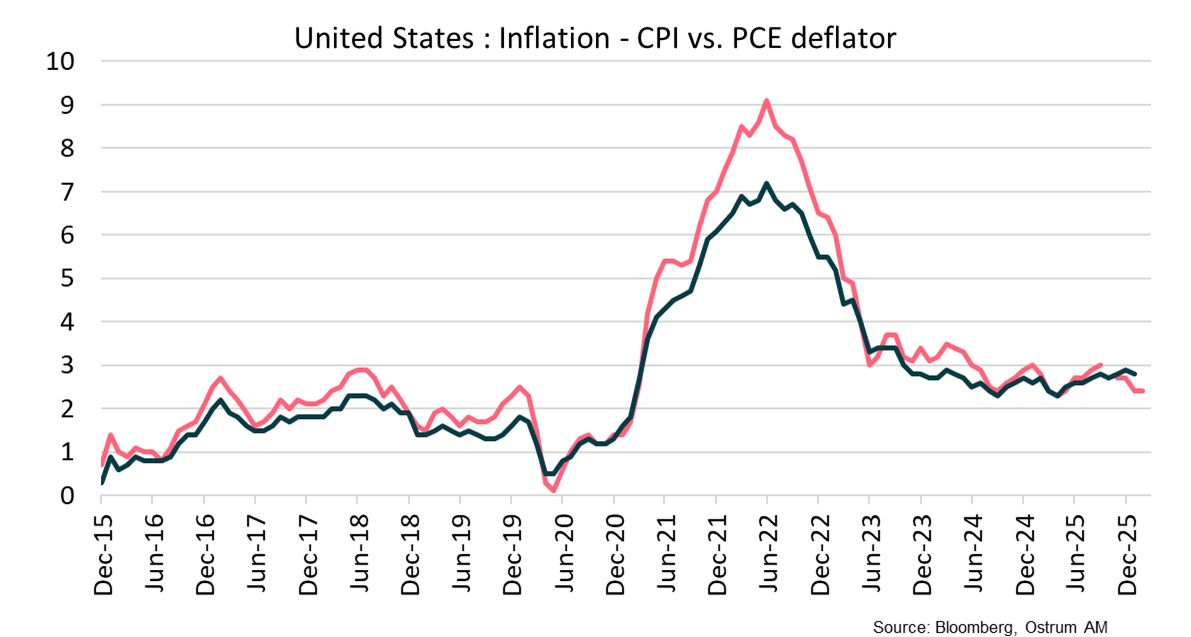

- PCE inflation remains elevated at 2.9% in February, but the Supreme Court ruling striking down tariffs could reduce inflationary pressures, despite temporary oil price increases from the Iran crisis.

- Policymakers are monitoring vulnerabilities related to leverage in hedge funds and life insurance companies, though public bond markets remain relatively stable despite widening credit spreads from recent volatility.

- March meeting expectations: The March meeting will be pivotal, with likely downward revisions to growth forecasts and a probable dovish Fed bias, prioritizing employment risks over inflation concerns given the dual mandate challenges.

The January status quo warrants rethinking

Status quo with 2 dissents in January

The January 28 FOMC statement and meeting minutes published a few weeks later indicated that the unemployment rate showed signs of stabilization as inflation remained somewhat elevated. The statement was notably shorter than in December, when policymakers added a paragraph explaining the rationale for reserve management purchases of Treasury bills to the tune of $40 billion per month. In the prior three FOMC, the Fed had eased considerably proceeding with successive 25-bp rate cuts, ending quantitive tightening and thus introducing bank reserve management.

Voting against the status quo on interest rates were Governors Stephen Miran and Christopher Waller, who preferred to lower the target range for the federal funds rate by 25 basis points at the January meeting. Whilst Stephen Miran kept showing loyalty to President Donald Trump by dissenting at every meeting since September, Christopher Waller argued that labor market developments required additional monetary easing.

The US labor market si no longer showing “signs of stabilization”

The labor market situation is worse than expected back in January

In late January, policymakers did not have the employment reports for January and February which showed continued sluggishness in job creation. In the three months to February 2026, the U.S. economy added a paltry 6k jobs per month on average. Though a strike in the health care sector distorted the February job data, it confirmed that the labor market has been at a standstill since last Spring and the Liberation Day tariff increases. Manufacturing firms shed 93k jobs since March 2025. Though consumer spending continued to expand during this period, the real disposable income of households has also declined.

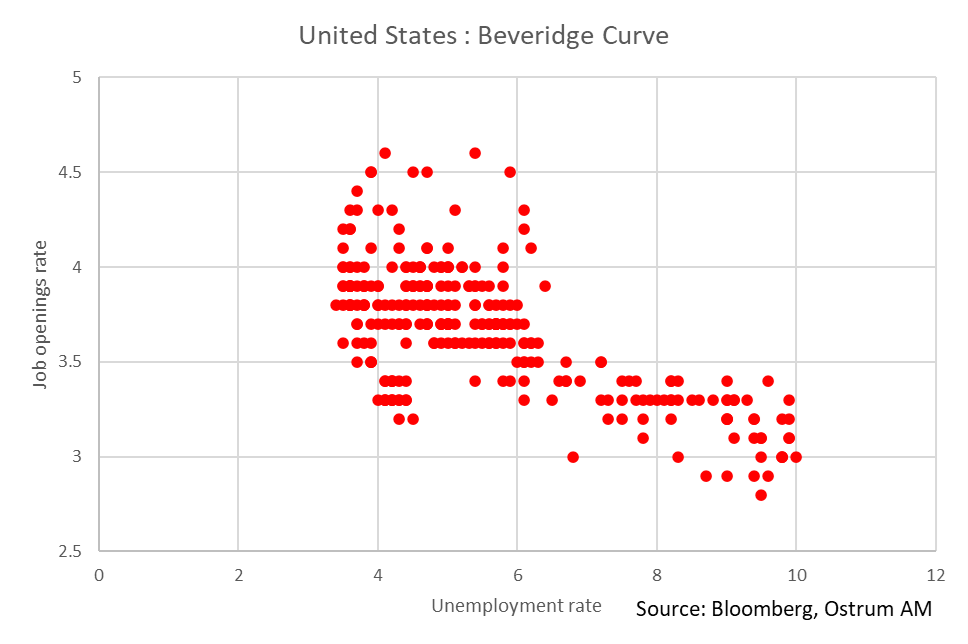

The job opening rate has now fallen below the level consistent growing imbalance in the labor market according to Governor Waller. The Beveridge curve – which depicts the inverse relationship between the job openings rate and the unemployment rate – suggests that further declines in job openings could be associated with faster rises in the jobless rate. This kink is right around the 4.5 % unemployment rate mark. Coincidentally, mass layoff announcements from the Challenger survey jumped in January (although UPS and Amazon account for a large share of staff cuts) whilst hiring announcements declined to a mere 5k. The unemployment rate increased to 4.4% in February despite declining labor market participation to 62%. At 4.4%, the jobless rate is in line with the Fed’s year-end projection. This suggests that further deterioration from current levels would likely require easing from the committee’s standpoint.

In addition, the annual revisions to population (included in the February employment report due to shutdown delay) estimates paint a bleak picture of the outlook for employment in years ahead. Unless massive AI investments spur lasting productivity gains, the U.S. potential GDP growth may slow below current estimates of 1.8%. Should potential growth slow, the Fed will lower its estimate for the steady-state or neutral Fed funds rate.

The inflation situation is harder to assess

Assessing the impact of oil price shocks

In January, the Fed noted that inflation remained elevated. The concern over upside risks to inflation reflected in part the ongoing impact of tariffs on consumer good prices. The Supreme Court ruling that determined that IEEPA tariffs were illegal may reduce the risks to inflation, even though President Donald Trump swiftly reimposed temporary 15% duties on all imports that will last until late July (and require Congress approval thereafter).

At 2.9% in February, the Fed’s preferred inflation measure - the PCE deflator – is running at uncomfortably high levels, nearly 1pp above the target. By comparison, the CPI report, released in advance of the deflator, stands at 2.4% in February. The gap between the two inflation measures is usually the other way around. PCE inflation has been consistently below CPI until recently. The lower weight of shelter expenditure in the PCE is the main source of difference. Rent disinflation thus has a larger impact on CPI. Healthcare costs also raise PCE inflation relative to CPI. In any case, most Fed policymakers will agree that inflation is too high.

The latest runup in oil prices following Iran strikes is harder to assess. Fed research would strongly suggest that the FOMC should avoid responding to higher crude prices as energy prices have both inflationary (in the short term) and disinflationary effects (in the medium term). Household real income will be dented further by higher gasoline prices ($3.60 per gallon). Having said that, the current energy shock is nowhere near the 2022 crisis, when national gasoline prices hit 5$, even topping $6.5 locally. The government is taking measures to facilitate oil transportation in the U.S. to mitigate the risk of local gas supply disruptions. Sanctions on Russian oil purchases have been waived temporarily. The Fed could take comfort in the announced release of strategic petroleum reserves worth 172 million barrels and the incentive for shale producers to add capacity. U.S. oil output hovers about multi-year highs at 13.6 million barrels per day.

The financial market situation has worsened, but not yet in crisis mode

Financial vulnerabilities are increasing

It may have stayed under the radar but the January FOMC minutes reveal that policymakers expressed concerns about financial stability: “Vulnerabilities associated with leverage in the financial sector were characterized as notable. Leverage remained high at hedge funds and life insurance companies. By contrast, bank regulatory capital ratios were high, although their market-adjusted capital ratios remained depressed and sensitive to long-term interest rates”. The footprint of hedge funds in Treasury markets and the importance of relative value or basis trades could make the market vulnerable.

Though market volatility has increased, the S&P 500 index is just 4% off its all-time high. Spreads have widened in synch with stock price declines. Spreads on U.S. investment grade corporate bonds trade at 134 bps vs. OIS undoing the late 2025 rally (spreads are 30 bps off January lows). The heavy issuance of technology corporate bonds was absorbed by credit markets and private credit market woes have had little impact on public bond markets so far. The U.S. dollar has strengthened as the greenback reclaimed its safe haven status. In sum, volatility from the Iran crisis has been concentrated in equity space, notably through increased demand for downside protection.

In addition, policymakers will take comfort in the increase in bank reserves. In December, the decided to engage in reserve management purchases of Treasury bills to lift bank reserve balances back above $3 trillion. Though there is no official target for aggregate reserve balances, the break below that threshold late last year did trigger a response from monetary authorities. We would not be surprised if net bill purchases are scaled back to say 20 billion a month sometime in the second quarter. MBS proceeds continue to be reinvested in short-term bills, which in itself provide ongoing relief.

Expected changes in the summar of economic projections

Market participants will closely watch the FOMC dot plot and the economic projections. Changes in the median Fed rate forecasts will move markets. The minutes showed that some participants consider that Fed funds rates (3.50-3.75%) were in the upper part of their neutral range already. There is a fair chance of increased disparity in rate projections for 2026 and years ahead. Some FOMC members, including Governor Waller, will stress the dire labor market situation, others will put the onus on the enhanced upside risks to inflation from the energy spike. On balance, we think an easing bias will stick. Growth forecasts could be adjusted lower (from 2.3% year-over-year in Q4 2026) amid downside risks from higher energy prices and weaker job creation. Headline inflation forecasts should be tweaked higher but market participants may pay more attention to core PCE inflation (currently forecasted at 2.5%).

Conclusion

The March meeting will be interesting considering the recent developments in Iran and weaker economic readings since January. The dual mandate of maximum employment and price stability makes the Fed’s job quite difficult in current circumstances. Financial developments pertaining to private credit market warrant monitoring. On balance, we believe that risks to growth and employment are greater than upside risks to inflation. Chair Powell may add comments on financial stability, which could be seen as a further dovish tilt.

Axel Botte

Chart of the week

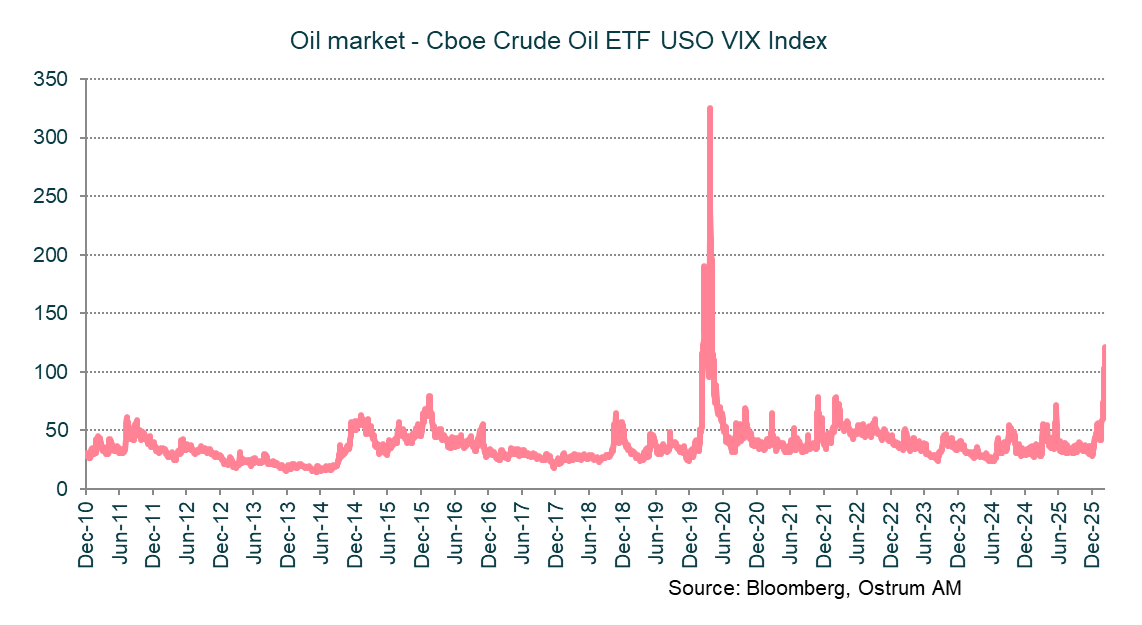

The military intervention led by the United States and Israel in Iran sent oil prices skyrocketing to around $100. The decision to release strategic oil reserves and messages from the US administration helped to stem the pressure on oil prices, but volatility in oil prices remains very elevated. Indeed, 16 oil cargoes have been hit by Iranian missiles, and the strait of Hormuz is de facto closed. Very few vessels can cross the strait. Oil production in the region has decreased considerably given the lack of storage capacity.

Looking at the “oil VIX”, the volatility shock is the largest since the Covid-induced collapse in oil prices.

Figure of the week

400

400 million barrels of strategic reserves of G7 countries will be released shortly to help reduce upward pressure on oil prices.

Market review:

- Iran crisis: the strait of Hormuz remains closed, G7 to tap oil reserves.

- United States: Q4 GDP revised down to 0.7%.

- Bonds: yields under pressure as oil prices spur inflation expectations.

- Equities: stock prices fall without panic amid wider credit spreads.

Financial Markets Navigate Through Uncertainty

A sustained closure of the Strait of Hormuz would present an insurmountable constraint to the global economy. Financial markets remain keenly attuned to developments emanating from the Middle East, temporarily overshadowing the risks embedded within the US private credit market.

The structurally bearish positioning against the dollar likely underpinned its recent rebound, despite the US administration's missteps in managing operations in Iran. Maritime traffic through the Strait of Hormuz has effectively ceased, with the exception of a handful of vessels bound for China and India. Risks to the global economy continue to accumulate, even with the announcement of releasing 400 million barrels from strategic petroleum reserves. However, this measure will only offset the halt in Gulf country exports for a few weeks at most. In this environment, with Brent crude exceeding $100 a barrel, interest rates are firming amid fears of renewed price acceleration. Equities have declined by 1.6% over the past week, as measured by the S&P 500. Demand for downside protection is increasing in the options market, yet the reaction of risk assets remains largely muted to date, considering the magnitude of economic risks.

On the macroeconomic front, US GDP for the 4th quarter has been revised downwards to 0.7% from an initial reading of 1.6%. Consumer spending on services and private investment were also revised lower. While an improvement in surveys and the end of the shutdown initially suggested a first-quarter rebound, activity is now likely to be constrained by rising energy prices. Gasoline prices are approaching $3.60, impacting household confidence. That said, residential construction is finally showing signs of recovery. The Fed is expected to acknowledge the growth slowdown and the weak February employment report. Inflation, however, remains elevated at 3.1% based on the core PCE deflator. In the Eurozone, the ECB is monitoring the surge in energy prices, amplified by the euro's decline below $1.15. Imported inflation may not jeopardize the status quo, but Christine Lagarde will reiterate her vigilance regarding upside inflation risks. The BoE faces an even more complex situation, given the acceleration of inflation sustained by wage growth since the start of monetary easing.

In bond markets, tensions are resurfacing in long-term yields. The 10-year US Treasury note is approaching the 4.30% threshold, while the German Bund is revisiting the 2025 highs of 2.94% reached following announcements of public investment in Germany. These movements coincide with the oil rebound and rising inflation expectations (+100 bps in 2-year inflation expectations for the Eurozone). The JGB market, and even more so the UK Gilt market, are also exhibiting fragility. The only safe haven appears to be the U.S. dollar, likely buoyed by currency hedge unwinds. On the equity front, the correction is resuming, albeit without panic. The S&P 500 has even traded within a very narrow range year-to-date, a historically tight band not seen in 60 years. Demand for downside protection has increased, supporting implied volatility (VIX at 30%), which in turn is fueling a rebound in credit default swap (CDS) index spreads. The iTraxx Crossover has moved back above the 300 basis points mark. The credit market, however, remains relatively calm and capable of absorbing large-scale issuance, such as that of Amazon. Investment-grade spreads stand at 78 basis points over swaps. Sovereign spreads are widening in parallel.

Axel Botte

Main market indicators