2025 Outlook

What Options Amid the Resurgence of Unpredictability?

The year 2024 is ending on a positive note, both in the bond and equity markets, despite the economic divergences between the United States and the rest of the world, as well as a persistently high floor on interest rates.

2025 is likely to present a complex landscape, marked by uncertainty stemming from the outcome of the US elections, and heightened inflationary and budgetary risks contributing to volatility in long-term rates, both in the United States and in Europe.

Against this unpredictable backdrop, Axel Botte, Head of Market Strategy, Alexandre Caminade, Head of Core Fixed Income and Liquid Alternatives, Philippe Berthelot, Head of Credit and Money Markets, and Frédéric Leguay, Head of Insurance Equity Management, present Ostrum Asset Management (Ostrum AM)'s outlook for the economy and markets, and the choices they believe should be made for 2025 to take advantage of the current environment.

Markets: facing up to the Trump administration

According to Axel Botte, Head of Market Strategy, Donald Trump's return to power heralds a return to unpredictability. US trade policy is set to tighten, with higher tariffs. China is in the line of fire, as are Canada and Mexico, even though they form a free trade zone with the United States under a trade agreement due for renegotiation in 2026. Higher tariffs will lead to higher prices for consumers, creating a source of uncertainty that could weigh on investment. According to Ostrum AM's scenario, US growth should fall below the 2% potential growth rate in 2025 (1.6%). Europe (1% in 2025) and China are also likely to suffer from Trump's tougher trade policy. However, there is budgetary leeway both in Germany and China to stimulate domestic demand. Retaliatory measures are also likely, in the form of customs tariffs or import quota restrictions (on US agricultural products, for example, in the case of China). Finally, it will also be important to distinguish noise from signal on immigration and climate policies: Donald Trump's announcements on the expulsion of millions of illegal immigrants and the priority given to fossil fuels are likely to collide with certain realities.

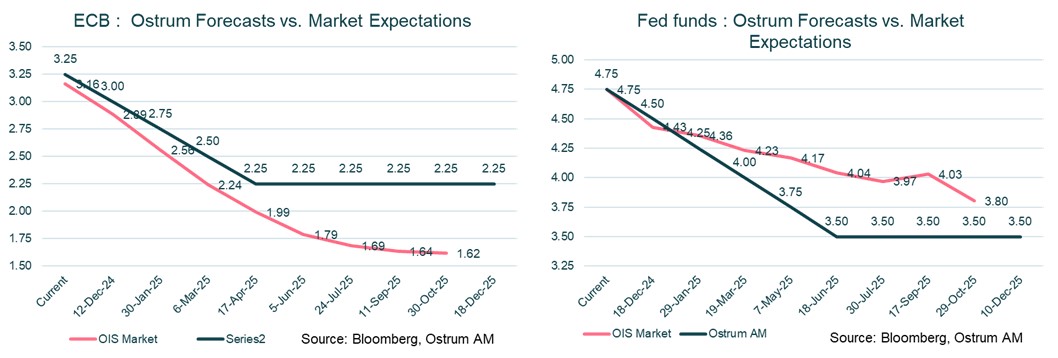

On the monetary front, the ECB is likely to reduce its rate to around 2.25% mid-2025 to mitigate the external shock by keeping the euro at around $1.05. The Fed, meanwhile, is likely to continue its steady easing, the extent of which will be limited by the effect of Trump's policies on inflation. Fed Funds should stabilise at around 3.50%, at the upper end of the neutral range. There are many risks to growth. In addition to trade policy, the tax cuts promised in the United States require a drastic reduction in federal spending to prevent the deficit from slipping towards 8% or 9% of GDP. This situation would put pressure on US long-term interest rates, likely to lead to a fall in risky assets.

Interest rates: high volatility and limited downside potential

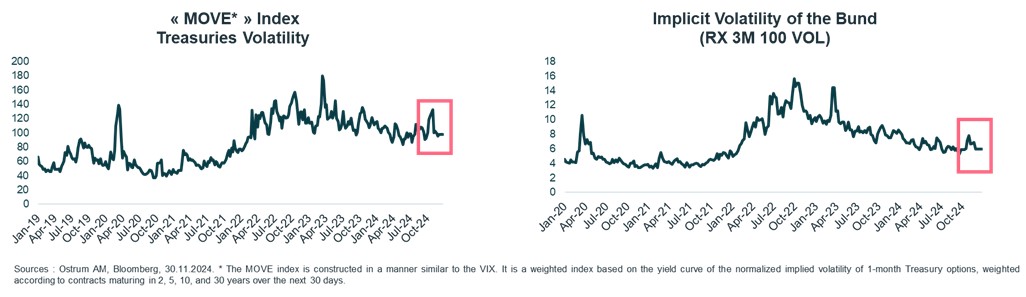

In 2025, the potential for rate cuts will remain limited in the United States and the eurozone. However, the uncertainty surrounding the implementation of the Trump administration's programme will continue to generate high volatility, particularly in US Treasury rates. According to Alexandre Caminade, Head of Core Rates and Liquid Alternatives, the increase in net issuances, especially in the eurozone in 2025, should weigh on the long end of the curve and justify a higher term premium. In the United States, this risk is more likely to materialise in 2026. Overall, Ostrum AM's teams forecast a 10-year rate of around 4.30% in the United States and 2.30% in Germany at the end of 2025. The breakeven inflation rates in the United States will continue to have upside potential due to doubts over the scale of the tariff hike. By contrast, the impact should be more limited in Europe.

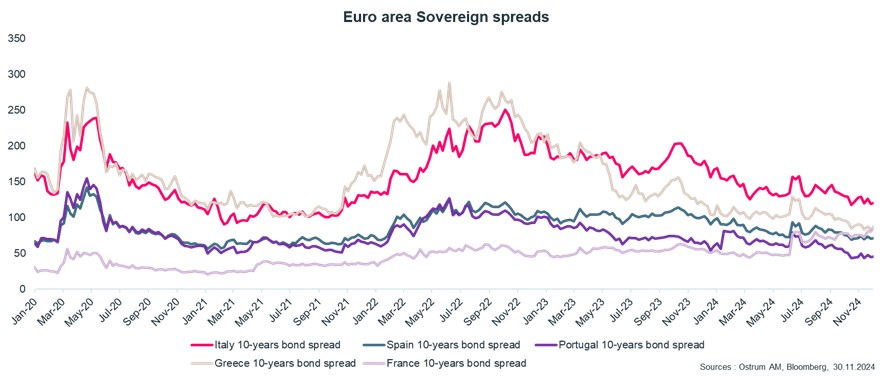

In sovereign spreads, a paradigm shift is taking shape, with an improvement in credit quality in the peripheral countries, while uncertainties persist in France and Germany. In addition to political uncertainty, these two countries will see their net issuances rise because of the accelerated reduction in the ECB's balance sheet with the end of reinvestments under the Pandemic Emergency Purchase Programme (PEPP). The spread between France and Germany is likely to fluctuate between 80 and 90 bp, with the risk of a negative outlook or even a downgrade by the rating agencies.

Swap spreads, which were particularly volatile at the end of the year, are expected to return to normal gradually, although the equilibrium level will be lower than in the first nine months of 2024.

Credit: 2025, a year of carry

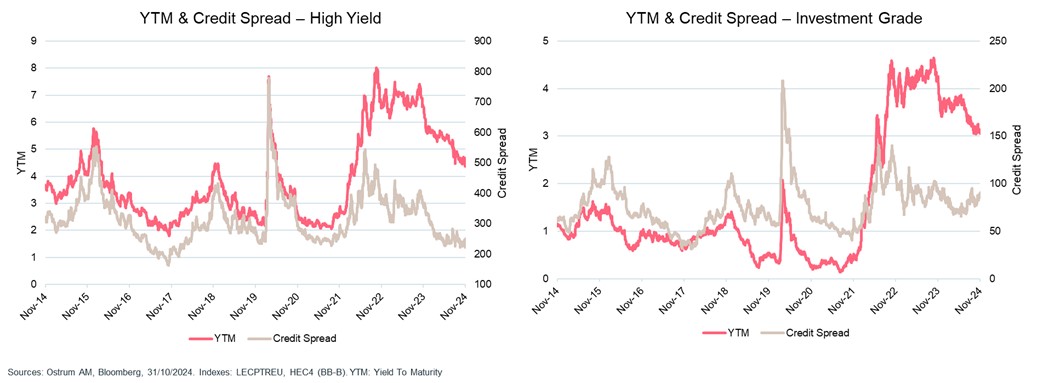

In 2025, Philippe Berthelot, Head of Credit and Money Markets, expects Investment Grade (IG) credit in Europe, whose spreads are in line with their 5-year average, to be mostly carried, unlike the High Yield (HY) segment, which looks set to become expensive over the same period due to attrition and volumes of rising stars well above those of fallen angels. US credit spreads are at their lowest for 20 years and are likely to underperform their European counterparts over the coming year.

Corporate leverage is under control, margins are high, and the default rate is expected to be below its historical average. These will remain supportive factors for the coming year. For example, Ostrum AM forecasts a GI spread of around 90 bp vs swap for euro credit at the end of 2025, similar to current levels. As for HY spreads, the teams expect a limited spread of around 50 bp, which is not enough to invert the performance hierarchy between these related asset classes. Sectoral allocation, which generally takes precedence over geographical allocation in a unified and homogenous currency zone, will be the focus of particular attention, given the growing political risk in certain core eurozone countries.

Ostrum AM prefers bank debt to non-financial corporate debt. These are more generous in terms of spreads and should benefit from a greater transformation effect thanks to even steeper yield curves. Credit should continue to see inflows, benefiting from historically attractive yields and even transfers of money market funds, which are becoming less and less remunerative due to multiple rate cuts by central banks.

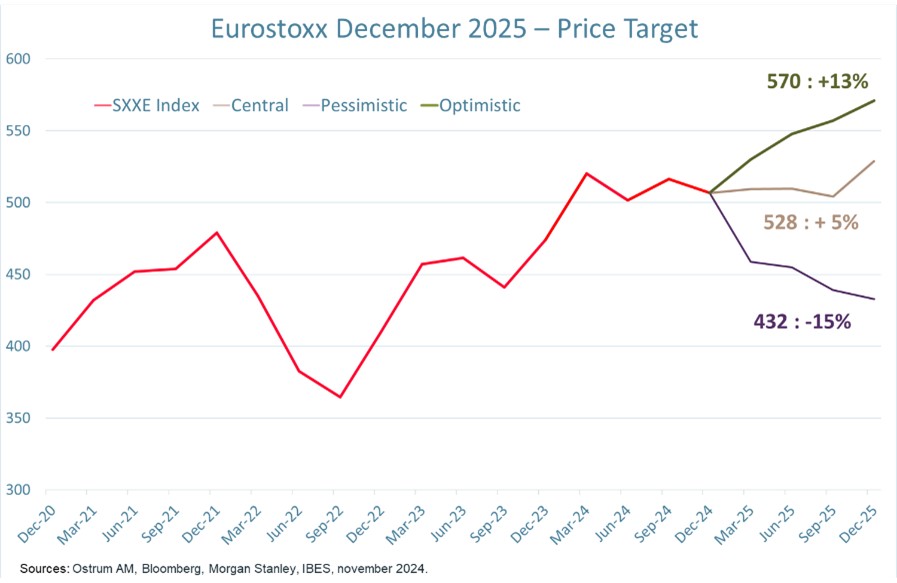

Equities: a trendless market in Europe awaiting clarification from the US

Buoyed at the start of 2024 by a US market that posted a performance of over 20% for the second year running, European markets are maintaining the lead they gained in the first quarter of this year, despite a difficult domestic and international environment. According to Frédéric Leguay, Head of Insurance Equity Management, 2025 should initially be driven by announcements from the United States, although the ECB's interest rate policy, developments in France and the elections in Germany will also influence the trend.

In 2025, European growth should stabilise, thanks to the ECB's monetary easing and the depreciation of the euro. Earnings, which are expected to decline slightly again in 2024, should rise in 2025, even if current expectations appear too high, particularly in those sectors most exposed to the cycle and to the Chinese economy.

Ostrum AM expects the earnings base in Europe to grow by 5%, which implies a downward revision of around 5 percentage points on analysts' expectations. As in the United States, but on a more reasonable scale, valuations in Europe have continued to rise in 2024. In the absence of a fall in profits, they do not give cause for concern. However, it will be necessary to keep a close eye on the direction of US long-term interest rates, and on the appetite for risk assets in the US, which has so far seemed insatiable.

European equity markets are likely to fluctuate, pending an assessment of the real economic impact of a first half rich in structuring events. However, short-term interest rates should continue to fall, and 2025 could also hold some pleasant surprises for an asset class that appears to be underweight.

To conclude, Gaëlle Malléjac, Global Chief Investment Officer at Ostrum AM, anticipates that With the return of unpredictability following the re-election of Donald Trump, investors are likely to face sustained volatility on the markets in 2025. However, by distinguishing current noise from plausible realities, Ostrum AM has identified several trends to guide its decisions: short-term real interest rates tending towards zero, leading to a gradual decline in the attractiveness of euro-denominated money market instruments as 2025 progresses; differing fiscal and inflationary risks, which will encourage investors to gradually reposition themselves towards longer maturities and countries whose situation is improving; an absence of recession and contained default rates, which should selectively benefit euro credit, both Investment Grade and High Yield quality, and give rise to opportunities on the European equity markets in the second half of the year.

The analysis and opinions expressed in this document represent the point of view of the referenced authors. They are issued on the date indicated, are subject to change and should not be construed as having any contractual value. This document is produced for information purposes only and should not be construed as an investment recommendation. Any investment may involve financial risk and should be carefully considered considering your financial needs and objectives. Ostrum Asset Management shall not be held liable for any decision taken or not taken based on any information contained in this document, nor for any use that may be made thereof by a third party.

Ostrum AM 2025 Outlook

Download the full PDF