Investing in ESG-focused bonds is a way to support the planet. While the sovereign bond market has limited issuers, it is still large and liquid, offering opportunities across the yield curve.

Highlights

- Sovereign bonds are sought after by investors due to regulatory constraints and a growing focus on sustainable investments.

- The sustainable bond market is maturing, making it an opportune time for investors to consider sovereign bonds as part of their allocation strategy.

- Ostrum Asset Management (Ostrum AM) employs proprietary research, best-in-class selection and engagement, prioritising alignment with sustainability goals.

Significant growth in the sustainable bond market has been driven by supply and demand dynamics. Notable accelerators are the Paris Agreement (2015) which led to the creation of the 17 United Nations Sustainable Development Goals or SDGs1, making it possible to measure investments by SDG contribution. The establishment of the Glasgow Financial Alliance for Net Zero or GFANZ (2021), with the aim to increase financing to reach a net-zero economy. As well as the amendments of national and supranational frameworks to include green and social expenditures as eligible programs for public financing. Such initiatives have influenced the CSR (Corporate Social Responsibility) strategies of European investors, encouraging them to make increased commitments to the green transition and social causes.

The sustainable bond market has matured into bond categories (green, social, sustainability ...) after being inaugurated by the AAA rated European Investment Bank (the EU’s lending bank) in 2007 with a €600 million Climate Awareness Bond. Its target was to allocate proceeds exclusively to eligible renewable and energy efficiency projects in support of the European Union’s policy goals to achieve greenhouse gas emission savings by 2030.

Illustration of the EIB’s sustainable bond issuance and size

Source: Ostrum AM and Bloomberg, January 2025.

For the European Union, October 2019 was also a key date, with the publication of the €1 trillion European Green Deal policy, setting plans to become climate neutral by 2050. With green bonds showcased as the key tool to fund projects for the NextGenerationEU program and social bonds for the SURE program2. Another notable date is December 2024 when the EU Green Bond Regulation entered into force, aiming to ensure high standards, comparability and alignment with EU taxonomy. The EU Green Bond designation is voluntary and now co-exists with the ICMA3 Green Bond Principles and other international sustainable finance initiatives.

In terms of total market size, green bonds are the largest segment of the sustainable debt market, representing 63% of total issuance ($970bn) in 20244. The total sustainable bond market size is over $5 trillion as of end-August 20245.

Sovereign Bonds attract investors

Institutional investors are largely drawn to sovereign bonds due to regulatory requirements mandating their investment in these assets, says Isabelle Sanson, Head of Sovereigns and Inflation bond management at Ostrum AM.

Sanson says there is demand for sustainable sovereign bonds to fulfill CSR engagements, continued demand from employee savings schemes which include sovereign bond allocations, as well as demand from investors seeking products with high sustainable investment ratios. Sanson explains that, according to Ostrum AM’s definition, sustainable sovereign bonds that are rated 1-7 (in Ostrum AM’s scale up to 10, 1 is the best rating) qualify as sustainable investments6.

Timothée Pubellier, Senior Portfolio Manager, co-managing Ostrum AM’s strategy dedicated purely to sustainable bonds – Climate & Social Impact bond,, adds that these bonds also have 3 specific characteristics that qualify them as impact investments: intentionality (finance projects that will generate a positive impact), additionality (create value-add for people and the economy) and measurability (evaluate the projects financed, comparing the results versus objectives set).

For Pubellier, the growing demand for sustainable bonds as an impact investment is evidenced in the amount of assets under management invested by Ostrum AM on the behalf of its insurance and institutional clients which rose from €25bn in 2022 to €42bn end-2024, representing a growth of 60% over a 2-year period. Observing demand for the asset class, Pubellier says it made sense for Ostrum AM to launch a standalone strategy, which it did in 2022, to respond to investors’ growing interest for sustainable investments.

The challenge of a limited issuer pool

While sustainable bonds are attracting interest from a range of investors, investing in the asset class comes with its own constraints. In particular, Bloomberg Green has raised concerns that the $64 trillion global market for sovereign bonds is largely inhospitable to sustainability-minded investing because there are only a limited number of issuers. In fact, Bloomberg Green reports that there are fewer than 160 sustainable sovereign bond issues globally compared with more than 70,000 corporate bond issues, which means investors risk a much more concentrated portfolio7.

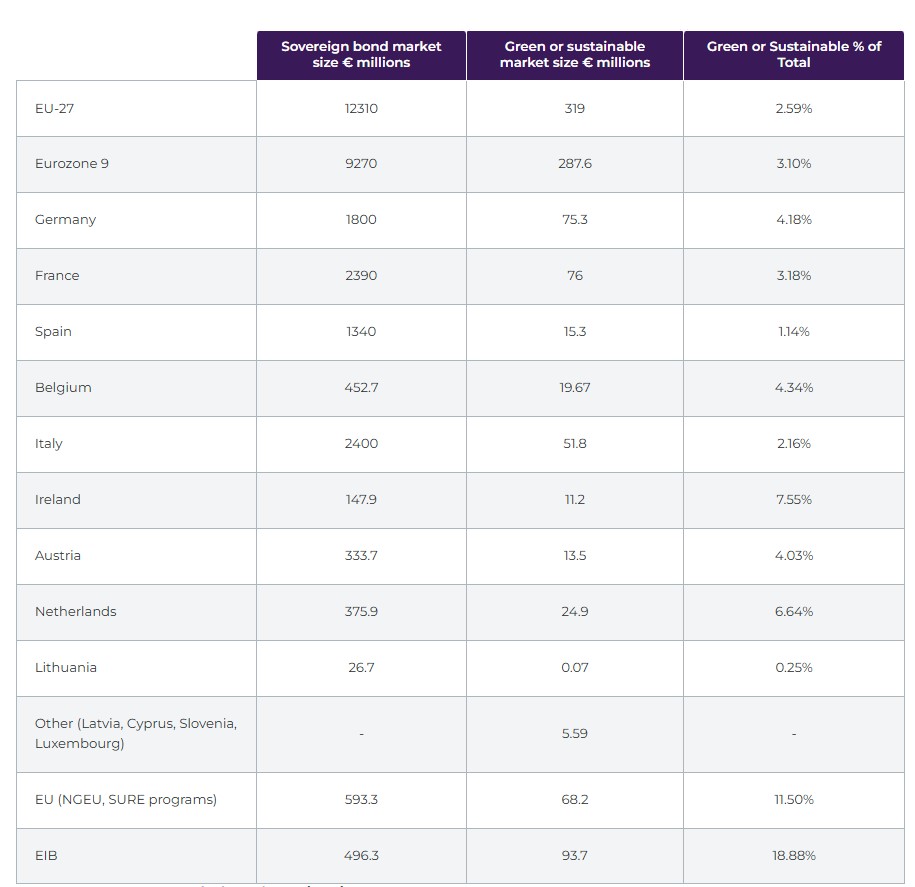

Sanson agrees that the limited number of sovereign issuers can pose a challenge, particularly since the European Union is made up of 27 countries with only a handful of countries issuing green bonds for a share of 2.6% of total bond issuance programs (source: Bloomberg). That said, if we consider the size of the EU-27 sovereign bond market is over €12 trillion, the 2.6% issued in green bonds represents a significant size, estimated at €319 bn.

Source: Ostrum AM and Bloomberg, January 2025.

Sanson illustrates how countries manage their green bond allocations, highlighting Germany’s framework, which was defined in 2020, relying on a concept of “twin bonds”. Here, conventional and green bonds are issued at the same time, with identical coupons and maturity dates. The only difference between the bonds is the size (the conventional bond size is significantly larger). Considering the green bonds come with allocation targets and KPIs, they could logically have a higher market value versus the conventional bonds, implying a greenium could emerge in the market. A greenium could also result from the smaller bond size (average bond issue size: €9bn for green versus €33bn for conventional). Germany’s green bonds (twin) issuance program includes short to very long maturities (2, 5, 10 and 30 year). In other sovereign sustainable bond markets, like Austria, Belgium, France, Italy, Ireland, Netherlands and Spain, bonds range from 5 to 30 years.

In terms of governance, each year, the various French ministries identify eligible green expenditure within their budgetary programs. Expenditures are submitted to the Green OAT Evaluation Council for opinion, then are submitted for validation to an interministerial steering committee. Eligible green expenditure is also selected on the basis of a green budget rating, in line with the Greenfin label reference framework, created by the French Ministry for Ecological Transition to attest to the green credentials of investment funds. France has issued 4 green OATs (sovereign bonds) to date, including an inflation linked bond, for an outstanding of over €70 billion. Funds are allocated as following: 32% to buildings, 17% to energy transition, 12% to transport, 7% to living resources (incl. biodiversity), 5% to adaptation to climate change, 27% to other initiatives (fight against pollution, eco-efficiency, transversal projects8. Use of Proceeds (UoP) are audited by an independent third party KPMG (recruited through a public tender offer) and rating agencies like Moody’s issues a second opinion.

For Sanson, when managing sovereign bond portfolios, the opportunity is in the bond picking across the yield curve. Of course, this opportunity was less evident when governments first started issuing, however, over the past few years, significant progress has been made to broaden the size of the universe, making it easier to manage sovereign bond portfolios.

Pubellier adds that for corporate bonds, sourcing bonds is not particularly challenging as the investment pool has become quite deep. Some European companies in the renewable energy and utilities sectors, for example, are now only issuing green bonds, providing good liquid options for thematic impact investing.

Pubellier agrees that the number of sustainable sovereign issuers is indeed concentrated with only 57 sovereign issuers globally, according to a July 2024 World Bank report. Although the number of issues is increasing, investors in the sovereign bond asset class will need to accept a certain amount of concentration.

Qualifying issuers with proprietary research

Pubellier highlights the need for “state of the art” tools for ESG-related bond analysis with seasoned analysts and portfolio managers who are trained to identify the best opportunities, explaining that Ostrum AM has developed proprietary tools that consider the specificities of each sustainable bond. Additionally, the firm applies sector & exclusion policies, as well as filters on “sustainable bonds” and “just transition”, reducing the investment universe for bond selection across the yield curve in all market segments (sovereigns, agencies, private sector) and targeting the best performance / ESG profile for portfolios.

Despite the challenges of having a limited number of issuers, thanks to opportunities in the yield curve, portfolios will have a reasonable number of issues (around 90 for a sustainable sovereign bond portfolio and around 130 for a sustainable aggregate bond portfolio) says Pubellier.

Ostrum AM’s expertise

Ostrum AM has an extensive track record of over 40 years in sovereign investing, along with its large assets under management in sovereign bonds (over €100bn, as at end-December 2024), positioning the firm to successfully address sustainable challenges. Ostrum AM proposes SFDR Article 8 sovereign solutions with high percentages of sustainable investments and embedded targets for ESG performance and reduced carbon intensity. Here, country selection is a major consideration for climate risk factors.

For Pubellier, co-manager of the the strategy dedicated purely to sustainable bonds – Climate & Social Impact bond,, bond selection has a Just Transition bias. This means, in addition to a rating on sustainable bonds, he also has a Just Transition indicator rating to consider when selecting bonds for the portfolio. A good Just Transition indicator rating ensures that social and local territorial engagements and KPIs are embedded in the projects financed by the sustainable bonds. For example, in the automobile sector, it is not enough to issue a green bond with the ambition to reduce CO2 emissions. Issuers must also make broader considerations, such as the impact on the millions of workers in factories or plans for recycling the existing fleet of cars, says Pubellier.

Finally, says Sanson, in line with the private sector, an additional and crucial step in our ESG approach to sovereign bonds is engagement. For Sovereigns, we started out engaging with a collaborate approach and then in 2023, we began rolling out our active individual engagement policy. To date, Ostrum AM has engaged with 13 countries (Greece, Ireland, Portugal, Australia, Italy, Germany, Spain, Indonesia, Austria, New Zealand, Singapore, Turkey, Japan), focusing on Sustainable Development Goals related particularly to SDG 7 (affordable and clean energy) and SDG 13 (climate action). These engagements are an opportunity for Ostrum AM to exchange with issuers on how they manage sovereign bond portfolios and how they select conventional and sustainable bonds based on ESG performance and carbon intensity attributes.

1 Created during the United Natioin sustainable development conference in Rio de Janeiro in 2012, and adopted in 2015.

2 NextGenerationEU program: a groundbreaking temporary recovery instrument to support Europe's economic recovery from the coronavirus pandemic SURE program: temporary Support to mitigate Unemployment Risks in an Emergency

3 ICMA : International Capital Market Association

4 Source: Ostrum AM, Bloomberg, 31/12/2024

5 Source: Climate Bond Initiative, août 2024.

6 https://www.ostrum.com/sites/default/files/1-ostrum-mediatheque/esg-rse/investissement-durable-definition-ostrum-am/Ostrum%20AM-%20Definition%20Sustainable%20Investments-EN.pdf

7 Source: Bloomberg, 31/03/2025

8 Source: Agence France Trésor, December 2023.