The investment community labels companies as growth or value, while also categorizing them by sector, geography, and themes. At times, catchy acronyms like the "Magnificent 7" emerge to highlight standout firms. Given the increasing dynamism of Asian Equity markets, employing a Corporate Lifecycle Framework provides an innovative approach to deconstruct the investment universe, refine one's stock selection, and strategically position for long-term success, ultimately gaining a competitive advantage.

Rushil Khanna is a seasoned emerging market investor, an active “bottom-up” stock picker. After starting off his career in 2004 at Credit Suisse HOLT's research labs in London, he has launched various global, regional, and thematic strategies based on value creation principles over the past 20 years.

Why focus on Asian equities now?

Rushil Khanna, our head of Asian Equities, based in Singapore, analyses the outstanding situation on this market currently: “There has been a powerful and spectacular shift in prevailing biases and market beliefs on Asia ex-Japan equities led by China in recent weeks and months”.

Indeed, China’s Hang Seng Tech Index is up close to 30% in USD terms YTD and over 70% in the last 12 months (as at 5 March 2025). The broader MSCI China index is up close to 45% in the last year and almost 20% YTD (as at 5 March 2025).

What has changed and more importantly is the rally sustainable?

We identify several catalysts in play:

- Regulatory: the roll out of friendlier pro-market policies from the Central Bank of the People’s Republic of China (PBoC).

- Fundamentals: corporate China is demonstrating signs of improving capital discipline with rising free cash flows, reduction in gearing, higher payouts and increasing share buybacks.

- Technology advances: the Artificial Intelligence leap, with the release of DeepSeek and equivalent models by Alibaba and Tencent, is ushering in a new sense of optimism.

Looking beyond China, other equity markets in the region, like India, have witnessed a correction over the past five months. We believe the correction in India is healthy as it is cyclical in nature. The country’s multi-year structural growth story is still intact. We expect the Indian economy to double in size from 2022 to 2031 which brings exciting opportunities from an investment perspective.

More largely, an allocation to the Asian equity markets offers investors portfolio diversification due to its low correlations to developed market equities.

Classification: an established tradition

Classifying companies began in the 1930s based on grouping companies with a “supply” side approach, focusing on the production attributes to categorize companies into industries such as agriculture, manufacturing, distribution, retail, and services. Later, more modern classification systems emerged, including The Refinitiv Business Classification (TRBC), The Industry Classification Benchmark (ICB), and the Global Industry Classification Standard (GICS), adopting a “demand-side” (market oriented) approach, focusing on products or services sold. Here, providers incorporate some discretion in their rules-based methodology to best represent business activities in their classification.

Style investing emerged with Value proclaimed as a distinctive style by Graham and Dodd in 1934 and then in 1937, T. Rowe Price surfaced to advocate Growth. Today, the market is segmented into various styles with many subscribing to the view that these philosophies are mutually exclusive. That said, some companies may have both Value and Growth properties while others may have neither.

Beyond standard classifications: the case for Life Cycle analysis

Classifications are market standards, providing visibility of portfolio positioning, and serving to evaluate investment performance relative to benchmarks. Rushil Khanna says these groupings tend to point to similarities across companies, whereas companies will each have very distinct features and drivers.

Within the traditional sector or industry group, for example, there are companies that are not competing directly, and some companies in the same group may operate in entirely different markets.

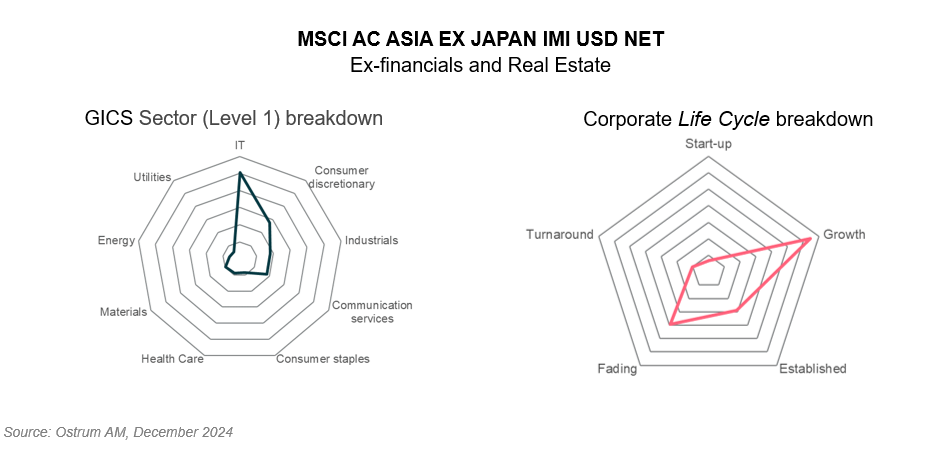

GICS1 versus Life Cycle classification

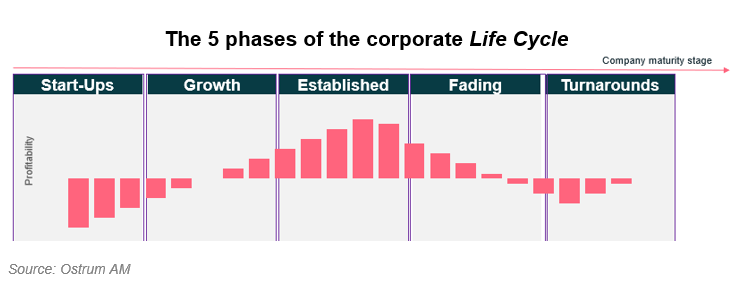

Rushil Khanna is convinced that Life Cycle classification gives his team an edge in Asia. He defines Life Cycle as a unique framework that categorizes companies into five stages of corporate maturity, allowing the team to select opportunities by stage. The aim is to identify, for example, firms that are ageing and may be ripe for a turnaround strategy, as well as those that demonstrate strong growth potential and still have a long runway ahead.

Recognizing that companies excel in various stages of their Life Cycle implies that value creation drivers differ by stage and that a company’s alpha drivers evolve over time. Active management identifies leading value creators by stage and adjusts positioning over time. For Rushil Khanna, the framework serves to guide the team in selecting the companies they want to hold and those they want to avoid.

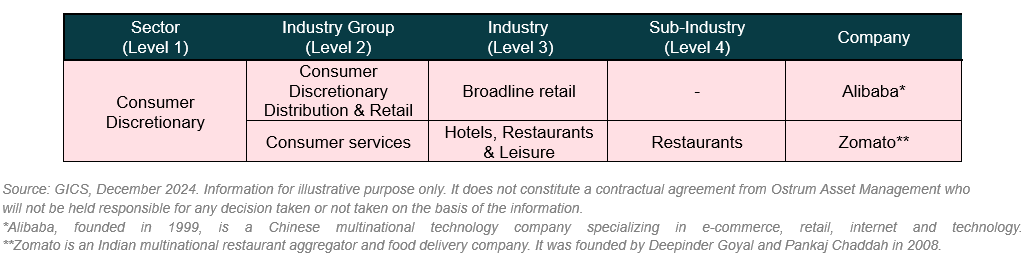

To illustrate how companies within the same GICS sector can differ when examining their business closely, Khanna’s team differentiate between two Asian companies operating in the ecommerce segment. Using a Life Cycle approach, these companies are classified differently: Zomato in India is categorized as a Start-ups stage company, while Alibaba in China is classified as Established. The value creation priorities for each are quite different and from a bottom-up perspective are analysed differently.

Does Life Cycle classification apply to all sectors?

For Rushil Khanna, the approach is beneficial for most sectors, with Financials and Real Estate treated apart as these sectors mainly use financial leverage, which implies they need to be treated differently versus other sectors. The team classifies the entire index into Life Cycle stages to better understand risks, to diversify holdings by maturity and to avoid making unintended positions. While a growth manager will typically hold positions in the early stages of the Life Cycle and value and dividend managers in the late stages, focusing on value creation by Life Cycle allows the team to diversify their positions.

Conclusion

In Asia ex-Japan, the investment universe is comprised of approximately 3,000 companies, which Rushil Khanna and team screen using a quantitative filter that integrates ESG criteria and an exclusion policy. This process narrows the universe down to about 200 best-in-class candidates classified by their maturity cycle. From this pool, they select early to late-stage companies, each characterized by unique attributes.

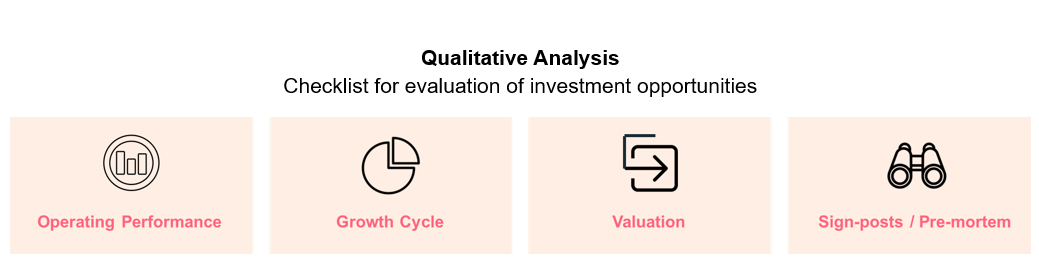

All candidates undergo a thorough analysis using a checklist that evaluates key indicators, including operating performance, ESG materiality2, performance relative to peers, valuation, and potential risks. The final portfolio targets 40-60 companies that pass both quantitative and qualitative due diligence. Sizing is based on factors such as liquidity, active weight, carbon intensity, sector, country, and Life Cycle limits.

For Rushil Khanna and team, the Life Cycle approach enhances confidence in their selection as well as serving to ensure that their selection is diversified across industries, ultimately leading to distinct portfolio attributes relative to peers. By employing this unique lens to rank companies, they believe they can better mitigate market risks and position themselves for outperformance relative to benchmarks.

The Ostrum AM Asia Equity team, NIM Singapore Ltd, is confident that this unique approach to Asian equity delivers a differentiate portfolio and therefore presents a compelling opportunity for investors.

1The GICS classification system prioritizes revenues over earnings to reflect a company's activities. Companies are assigned to a Sub-Industry based on the majority of their revenues; those active in three or more sectors are classified as Industrial Conglomerates or Multi-Sector Holdings.

2Focus is on sustainability challenges that influence each company’s business sector or business model. The aim is to ward off potential risks and identify opportunities.